Using trusts is becoming increasingly common in financial planning. Trusts can make sure that your wealth is distributed to your chosen beneficiaries and can also help to ensure that they are not subject to Inheritance Tax (IHT).

How can trusts help with financial planning?

Trusts can be set up to provide during your lifetime, a lifetime trust, or as part of your Will on death, a Will trust.

Putting something in trust, can avoid a delay in benefits being paid out and may help to reduce IHT. Currently IHT is payable at a rate of 40% on estates valued over £325,000, although gifts to your spouse or civil partner are not subject to IHT. However using trusts and with careful financial planning, the value of your estate can be reduced which will mean more of your wealth is passed to your chosen beneficiaries. An additional nil-rate band of £175,000 is available if a home is being passed to a direct descendant.

A trust can also be used with a protection plan to make sure your family has funds available to pay any IHT liability. This will stop the beneficiaries having to borrow funds or even sell the family home to pay any tax owed after you die.

What is a trust?

A trust is a way of choosing who will receive the benefit of certain assets, without giving your beneficiaries full and immediate control over them.

A trust is usually created by a trust deed – which will set out the terms of the trust. Within a trust there will be:

• The settlor or donor, this is the person creating the trust

• Trustees, these are the people who manage the trust on behalf of the beneficiaries (there should normally be at least two trustees)

• Beneficiaries who will receive the assets of the trust.

If the trustees break the terms of the trust, the beneficiaries may take legal action against them. It is important that you choose the trustees carefully as they are the legal owners of the assets within the trust and responsible for making sure these assets provide for the chosen beneficiaries in accordance with the trust deed.

What options are available?

There are many different types of trust, but the most common ones include:

Bare trusts are used to hold assets on named person’s (or persons’) behalf until they choose to take ownership. For example, bare trusts can be used to keep assets gifted to a child until they’re grown up. Assets placed in a bare trust are treated as potentially exempt transfers, which means that you will pay no IHT when establishing the trust, but if you die within seven years of creating it, the original amount of the gift will be added back to your estate to calculate IHT. Under a bare trust, the beneficiary has a legal right to the trust assets on reaching the age of 18 and therefore this type of trust may not provide the control and flexibility desired by the settlor.

Discretionary trusts hold assets which are then used for beneficiaries at the discretion of the trustees, in accordance with your intentions which are set out in the trust deed. As with bare trusts, if you survive seven years, the amount is excluded from the value of your estate for IHT.

Investment bonds are a useful vehicle to hold within a trust as they can make the trust simple for the trustees to administer. For example, as a bond does not produce any income (and therefore any liability for the trust to pay Income Tax) this means that the trust does not generally have to complete an annual tax return.

Depending on your circumstances, there are different ways in which investment bonds can be held, such as:

Gift trust – You can make an outright gift of capital to the trust and this can then be held by the trustees for the future benefit of the beneficiaries. This type of trust may be suitable where you will not require any access to the funds in the future.

Discounted gift trust – This type of trust allows you to make a gift of capital to the trust whilst retaining the right to receive regular payments of up to 5% each year of the original value of the gift for the remainder of your lifetime. The right to these regular payments gives an immediate discount to the estate, with the remainder of the gift falling outside the estate after seven years.

Loan trusts – You lend a capital amount to the trust, which means that the amount of the loan outstanding at the date of death will still form part of your estate when calculating IHT. However, any investment returns on the loan capital will be owned by the trust and be outside of your estate for IHT purposes. You can receive regular loan repayments or have capital repaid to you as and when required.

Alternatively you may decide to waive the loan capital at a future date. If you do so, then this would be treated as a gift and start the seven year clock for IHT from the date the load is waived.

There are also trust options for business protection policies and for employees using relevant life plans and these policies must be written in trust from the outset.

Preparing for long term care costs

Many clients are concerned that putting assets into a trust may limit their access to funds for any long term care needs in the future. When long term care is needed, the local council will carry out a financial means test of income, savings and property to see if they can support the costs either partly or in full.

Settlements into lifetime trusts can be regarded as a ‘deliberate deprivation of assets’ if it can be evidenced that the motivation for the gift was to avoid care home fees. If assets are regarded in this way, they may be included in their financial means test.

A flexible reversionary trust can provide a solution. Under this trust assets are gifted to the trust, which starts the seven year potentially exempt transfer clock, but allows the Trustees to make flexible periodic payments to support the financial needs of the settlor, for example to meet long term care costs if the need arises.

Payments can be made to other beneficiaries at the trustees’ discretion and in accordance with any letter of wishes of the settlor and under the discretionary powers set out in the trust deed.

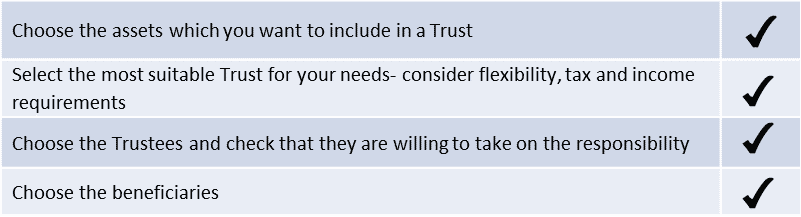

What should I consider in setting up a Trust?

Trusts are a valuable financial planning tool and you should ask your adviser how a trust could help you towards your goals. Once you and your adviser have discussed your requirements and decided what type of trust best matches your financial goals and your circumstances, you should regularly review that the trust remains suitable and reflects any legislation changes. Our advisers can demonstrate how a trust can preserve your wealth or if you are a trustee, we can help you to fulfil your responsibilities towards the beneficiaries of the trust.

CA5450 Exp 04/2021